Bet365 Free Bets Club: Weekly Tokens That Supercharge UK Punters' Weekend Wagers

14 Mar 2026

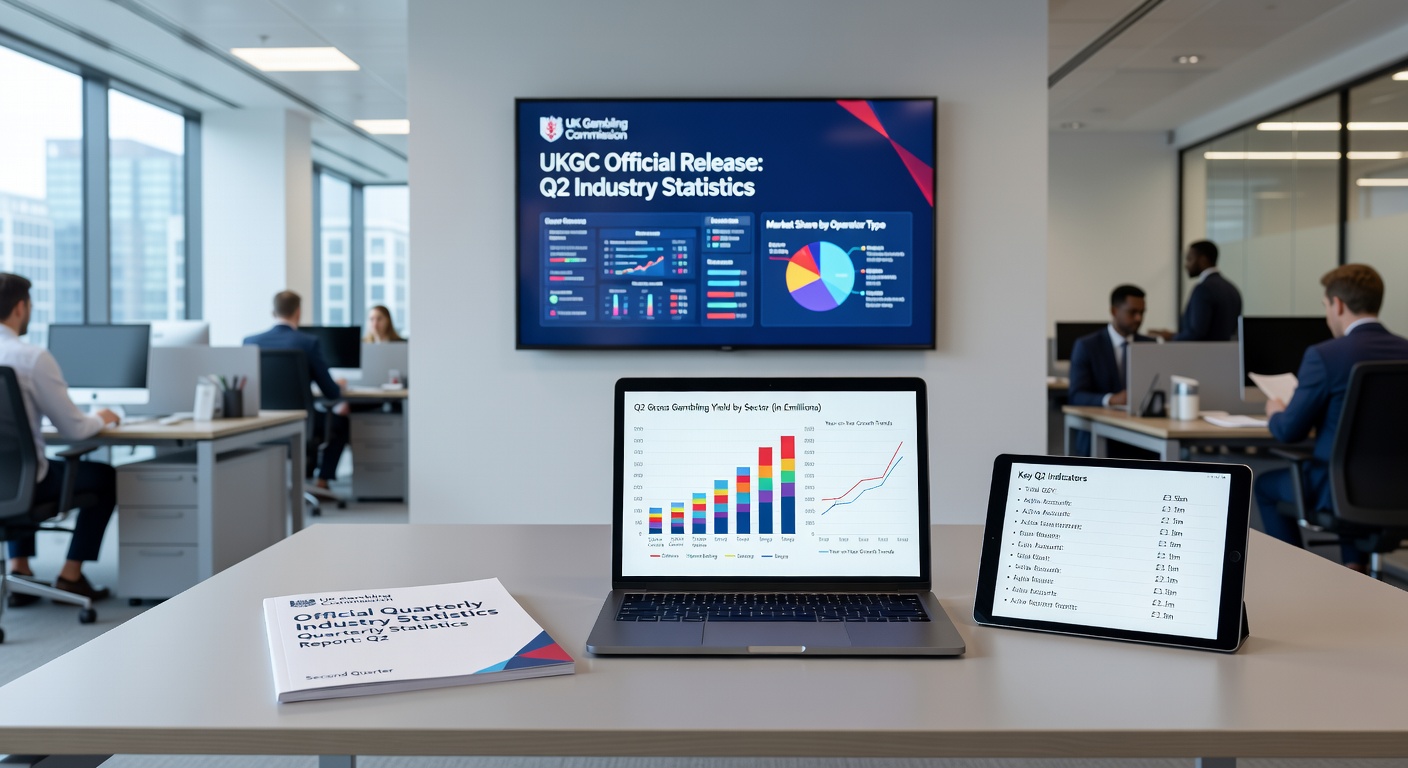

UK Gambling Commission Drops Q2 2025 Stats: Non-Remote Betting Clocks £592 Million GGY While Remote Sectors Hit £2 Billion Mark

The Latest from the Gambling Commission's Quarterly Report

Observers tracking the UK gambling landscape turned their attention to the UK Gambling Commission's official quarterly industry statistics for the second quarter of the financial year April 2025 to March 2026, a period spanning July to September 2025, and what those figures reveal about betting trends across Great Britain stands out sharply, especially now in March 2026 as the full year wraps up. Data highlights key shifts in both remote and non-remote sectors, with non-remote betting generating £592 million in Gross Gambling Yield—or GGY, the standard measure of operator profits after player winnings—and that chunk representing a solid 48.2% of the total non-remote GGY, all while 5,782 active betting shops kept the high street presence steady. Turns out the remote casino, betting, and bingo sector pulled in a hefty total GGY of £2.0 billion during the same window, and remote betting played a big role in driving those numbers higher, underscoring how digital platforms continue reshaping the industry's core dynamics.

Experts who pore over these reports note how GGY serves as the go-to metric for gauging sector health, since it captures stakes minus payouts and duties, giving a clear snapshot of where the money flows, and in Q2 2025, betting emerged as the linchpin connecting physical shops to online realms. People familiar with past quarters have seen remote growth accelerate, but this latest batch confirms the pattern holds firm, with non-remote betting not just hanging on but claiming nearly half of its category's yield despite fewer venues overall. And here's where it gets interesting: those 5,782 active betting shops—down slightly from prior periods in some spots, yet resilient—funneled £592 million into the economy through GGY, a figure that speaks to punters' enduring pull toward in-person wagering on everything from football matches to horse races.

Non-Remote Betting Holds Ground with £592 Million GGY

Non-remote betting, the backbone of traditional high street gambling, clocked in at £592 million GGY for July through September 2025, accounting for 48.2% of the broader non-remote total, and researchers digging into the data point out how this share reflects betting's dominance over slots or other activities in physical locations. With 5,782 active betting shops dotting Great Britain, operators maintained a network that supports local economies, draws crowds for live events, and keeps the tactile thrill of placing a bet alive, even as online options proliferate. Data shows this GGY figure stems from a mix of sports wagering—think Premier League openers or autumn racing festivals—where punters favor the atmosphere of a bustling shop, chatting odds with staff or watching screens light up with results.

What's notable here is the stability; those 5,782 shops represent a slight dip from peak numbers years back, but the yield per shop hovers efficiently, suggesting operators adapt by focusing on high-margin events, and observers who've tracked closures note how surviving venues cluster in urban hubs or near tracks, optimizing footfall. Take one case from the stats: betting shops contributed steadily without the volatility seen in other non-remote categories, holding 48.2% sway because GGY calculations factor in everything from over-the-counter singles to multi-leg accumulators, all processed amid the buzz of real-time action. That said, the £592 million doesn't exist in isolation; it ties into duties paid to the Treasury, fueling public coffers while operators reinvest in tech upgrades like faster terminals or self-service kiosks.

So while remote alternatives tempt with convenience, non-remote betting's GGY underscores a loyal base—weekend warriors, regulars nursing a pint and a punt—who keep shops viable, and as March 2026 approaches with FY end in sight, these figures offer a benchmark for what's sustained the sector through regulatory tweaks and economic headwinds.

Remote Sector's £2.0 Billion Milestone, Powered by Betting

Shifting gears to the remote side, the casino, betting, and bingo combo racked up £2.0 billion in GGY over Q2 2025, a total that dwarfs non-remote efforts and highlights digital's ascent, with remote betting emerging as a key driver amid smartphone ubiquity and 24/7 access. Figures reveal how this sector thrives on mobile apps, where users wager from sofas or commutes, placing bets on global sports without leaving home, and the Gambling Commission's breakdown shows betting's slice fueling much of that £2.0 billion, blending casino spins with bingo rooms into a remote powerhouse. Experts analyzing the trends observe how GGY here benefits from lower overheads—no rents or staff like shops demand—allowing operators to offer sharper odds or promotions that pull in younger demographics.

But here's teh thing: remote betting's significant contributions mean sports-focused platforms captured punter dollars alongside slots and cards, creating a hybrid appeal where one app handles football futures, virtual races, and live in-play markets, all contributing to the hefty yield. Data indicates this £2.0 billion reflects stakes poured into diverse remote activities, yet betting stands tall because seasonal events like early NFL or cricket internationals spike volumes, and those who've studied user patterns know how seamless deposits via cards or wallets keep sessions rolling. Interestingly, the remote bingo element adds variety—social chats amid number calls—while casinos draw high-rollers, but betting glues it together with broad accessibility.

Now, as the financial year nears its March 2026 close, these stats prompt questions about sustainability; remote GGY's scale suggests operators scale servers and compliance teams accordingly, handling surges from major tournaments, and the £2.0 billion mark serves as a milestone, especially since prior quarters hinted at this trajectory without confirming the betting-heavy push.

Betting Trends Bridging Remote and Non-Remote Worlds

Betting trends weave through both sectors in the Q2 data, with non-remote shops at 48.2% of their GGY pie via £592 million and remote betting bolstering the £2.0 billion total, revealing a tale of convergence where punters mix channels seamlessly. Researchers note how in-play betting explodes remotely—odds shifting live during matches—while shops excel in consultative parlays, staff guiding complex bets that boost GGY through higher margins, and the 5,782 active venues ensure no one's left without a local option. Turns out football dominates, per patterns in the stats, followed by horses, with greyhounds or tennis filling gaps, creating a year-round pulse that remote mirrors at scale.

One study-like insight from the report: active shop count holds at 5,782 because closures hit weaker spots, but survivors thrive on loyalty programs or hybrid models linking to apps, blurring lines further, and remote's edge comes from data analytics predicting bets, personalizing offers that nudge GGY upward. People who've compared quarters see betting's consistency—non-remote steady, remote surging—as the industry's North Star, resilient to stake limits or ad bans, and with March 2026 looming, operators eye Q4 for World Cup qualifiers that could echo Q2's vigor.

Yet the real story lies in the numbers' interplay; £592 million non-remote pairs with remote betting's lift to hit £2.0 billion sector-wide, showing betting's not just surviving but steering the ship, whether via till slips or touchscreens.

Implications for Operators and Regulators in 2026

Operators parsing the Gambling Commission stats adjust strategies based on these Q2 realities—bolstering the 5,782 shops with digital integrations or doubling down on remote betting to chase that £2.0 billion momentum—and data underscores how GGY splits inform boardroom calls, from shop refits to app enhancements. Regulators, meanwhile, use the figures to calibrate protections, noting 48.2% non-remote reliance signals shop-floor safeguards matter, while remote's scale demands robust age verification and self-exclusion tools. As March 2026 hits, with FY data compiling, these July-September insights shape